Final Countdown: Your Year-End Contribution and Transaction Deadlines

December is a good time to review deadlines for contributions, distributions, charitable giving, and account updates. Many account actions must be completed before December 31 to realize their tax benefits in the current year. Here’s your year-end financial checklist.

IRA and SEP-IRA Contributions

Deadline: December 31, 2025

– Traditional IRA contributions

– Roth IRA contributions

– Backdoor Roth conversions

Note: You have until April 15, 2026 (tax filing deadline) to make prior-year contributions, but to claim them on your 2025 taxes, they must be received by December 31.

401(k) and 403(b) Deferrals

Deadline: December 31, 2025 (employer payroll cutoff date varies)

Elective deferrals (employee contributions) must be withheld from your last paycheck of the year. Check with your HR department for the payroll cutoff date, as it may be before December 31.

Employer Profit-Sharing and Matching Contributions

Deadline: Varies by plan (typically December 31 for calendar year plans)

While employee deferrals have a calendar-year deadline, employer contributions can sometimes be made until the tax filing deadline with an extension. Check your plan documents or contact your employer.

Charitable Giving

Deadline: December 31, 2025

To claim a deduction on your 2025 tax return:

– Cash donations must be paid by December 31

– Non-cash donations must be delivered (not mailed) by December 31

– Checks written before year-end but postmarked after January 1 may not qualify

Consider these strategies:

– Donor-Advised Funds (make contribution by 12/31, recommend distributions later)

– Appreciated securities (avoid capital gains taxes)

– Qualified charitable distributions from IRAs (if age 70½+)

Required Minimum Distributions (RMDs)

Deadline: December 31, 2025

If you’re age 73 or older:

– Must withdraw from traditional IRAs, SEP-IRAs, and 401(k)s

– Failure to withdraw results in a 25% penalty on the amount not withdrawn (reduced to 10% if corrected timely)

– Exceptions exist for still-employed individuals and certain plans

Roth Conversions and Transfers

Deadline: December 31, 2025

– Roth conversions must be completed and reflected in your account

– Trustee-to-trustee transfers for account rollovers

– 60-day rollovers (be careful—strict deadline rules apply)

Estimated Quarterly Tax Payments

Deadline: December 31, 2025 (Fourth Quarter)

If you’re self-employed or have significant non-withheld income:

– Make your Q4 estimated tax payment by year-end

– Failure to pay can result in penalties and interest

Flexible Spending Account (FSA) and Dependent Care Account Elections

Deadline: Typically December 31, 2025

– FSA and dependent care account contributions must be claimed by year-end

– Unused balances may be forfeited (though some plans offer grace periods)

– Changes to elections generally require a qualifying life event

Charitable Remainder Trust (CRT) and Donor-Advised Fund (DAF) Contributions

Deadline: December 31, 2025

– Contributions must be completed to claim deductions in 2025

– Documents must be signed and funded

Investment-Related Deadlines

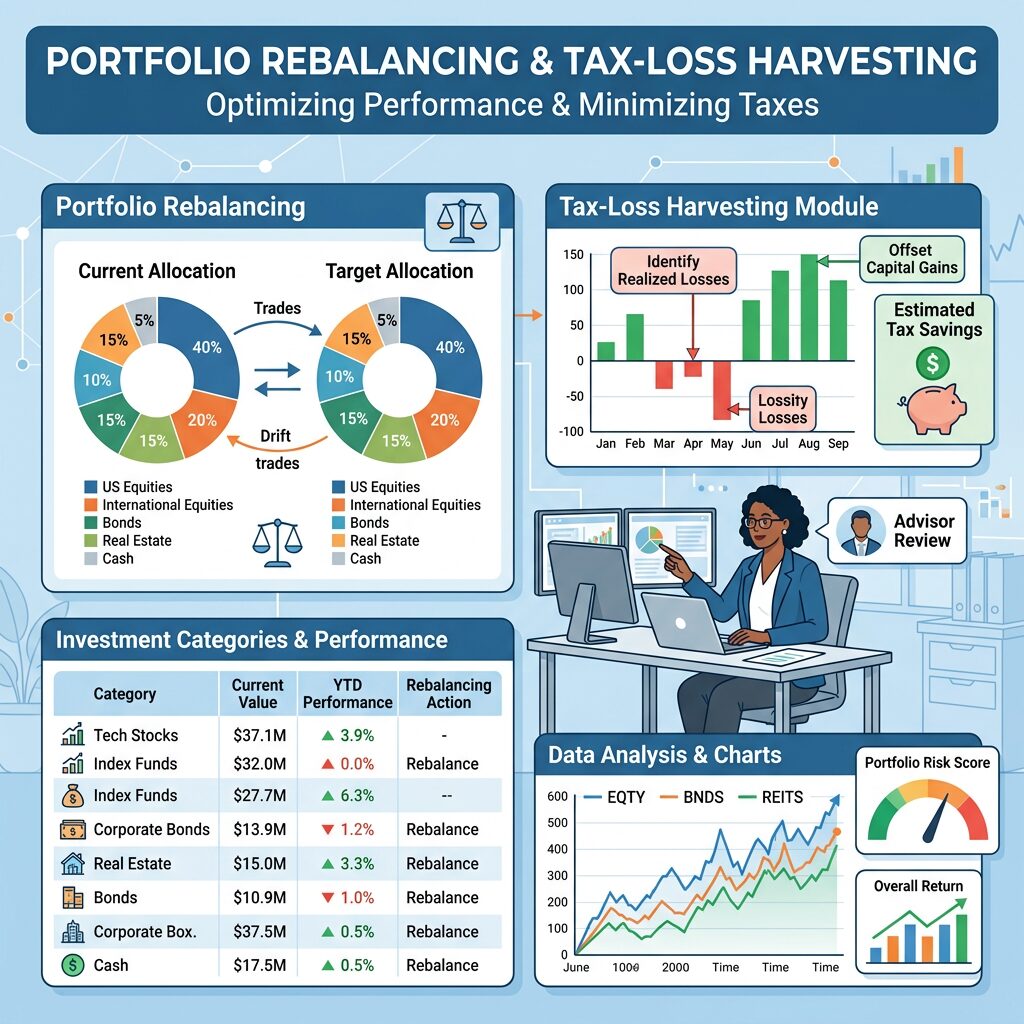

Tax-Loss Harvesting: December 31, 2025

– Sell securities with losses to offset gains

– Remember the 30-day wash sale rule

Rebalancing: By year-end

– Adjust portfolio allocations for tax efficiency and risk management

Year-End Planning Checklist

□ Check tax withholding on W-4 or quarterly estimates

□ Review retirement account contributions (have you maxed out?)

□ Consider Roth conversions

□ Plan charitable giving

□ Execute tax-loss harvesting

□ Verify all distributions and rollovers are processed

□ Update beneficiaries on retirement accounts

□ Review insurance coverage

□ Document investment cost basis

Don’t Miss These Opportunities

Year-end planning doesn’t have to be overwhelming. The key is addressing these items proactively rather than scrambling at the last minute. At Austin Wealth Management, our team can help you navigate these deadlines and implement strategies that align with your overall financial goals.

Schedule a consultation with us before year-end to ensure you’re taking full advantage of 2025’s tax planning opportunities and positioning yourself well for 2026.

More Articles

Trump Savings Accounts

The 2025 passage of the One Big Beautiful Bill Act introduced the Trump Account, a unique custodial investment tool designed to jumpstart savings for young Americans. For nearly three decades, families have relied on 529 plans...

How Portfolio Rebalancing and Tax-Loss Harvesting Help Austin Wealth Management Improve Client Outcomes

Behind every AWM advisor is a dedicated team of investment professionals meticulously looking at each client account and watching for opportunities to improve our clients investment performance...

Accessing Your 2025 Tax Documents

Your 2025 tax forms are available for download from Charles Schwab. If you opted to receive your tax documents by mail, they should arrive soon. How to Access Your Tax Forms Online: Charles Schwab Client Portal...