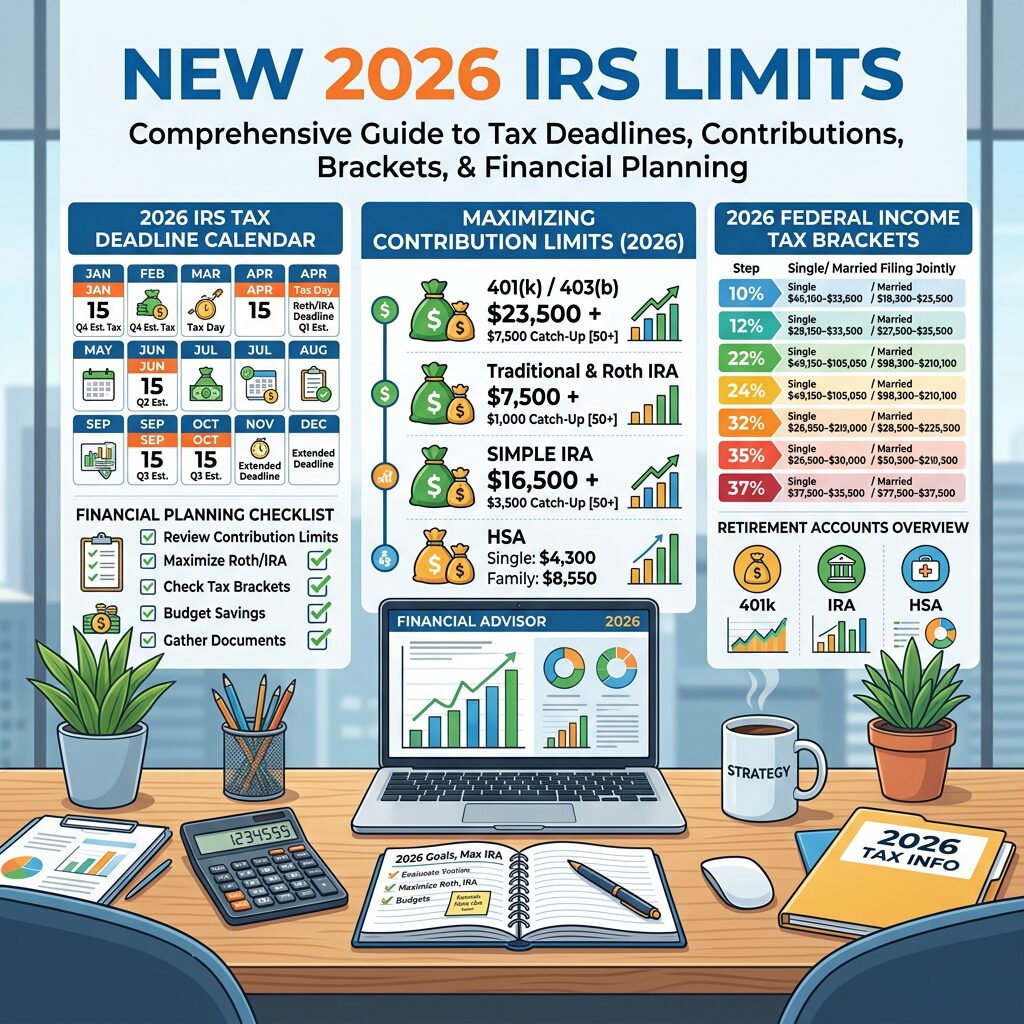

New 2026 IRS Limits: Bigger Breaks, Bigger Planning Opportunities

The IRS and Social Security Administration have released key numbers for 2026, including new federal income tax brackets, a higher standard deduction, bigger retirement and HSA contribution limits, and more. Here’s what changed and how you can take advantage.

2026 Standard Deduction

The standard deduction increases for all filing statuses:

– Single: $14,600 (up $350)

– Married filing jointly: $29,200 (up $700)

– Head of household: $21,900 (up $500)

– Married filing separately: $14,600 (up $350)

If your income falls below these amounts, you may not need to file a federal tax return.

2026 Tax Brackets

Federal income tax brackets are adjusted for inflation annually. For 2026, the brackets increase slightly, meaning some income that was previously taxed at a higher rate may now be taxed at a lower rate. This is especially important for strategic year-end planning.

Retirement Contribution Limits for 2026

Good news for savers!

401(k), 403(b), and Most 457 Plans:

– Employee deferrals: $24,500 (up from $23,500)

– Catch-up contributions (age 50+): $8,500 (unchanged)

– Total: $33,000

Traditional and Roth IRAs:

– Contribution limit: $7,000 (unchanged)

– Catch-up contributions (age 50+): $1,000 (unchanged)

– Total: $8,000

Health Savings Account (HSA):

– Self-only coverage: $4,300 (up from $4,150)

– Family coverage: $8,550 (up from $8,300)

– Catch-up contributions (age 55+): $1,150 (unchanged)

Social Security Updates

Full Retirement Age: Continues to gradually increase. Those born in 1959 have a full retirement age of 66 years and 10 months.

Maximum Taxable Earnings: $174,900 (up from $168,600 in 2025), meaning self-employed individuals and employees pay Social Security taxes on earnings up to this amount.

Planning Strategies for 2026

1. Maximize Retirement Contributions

With higher contribution limits, increase your 401(k) deferral or IRA contributions to take advantage of tax-deferred or tax-free growth.

2. HSA Prioritization

If eligible, max out your HSA. It’s the only account that offers triple tax benefits: contributions are tax-deductible, growth is tax-free, and qualified distributions are tax-free.

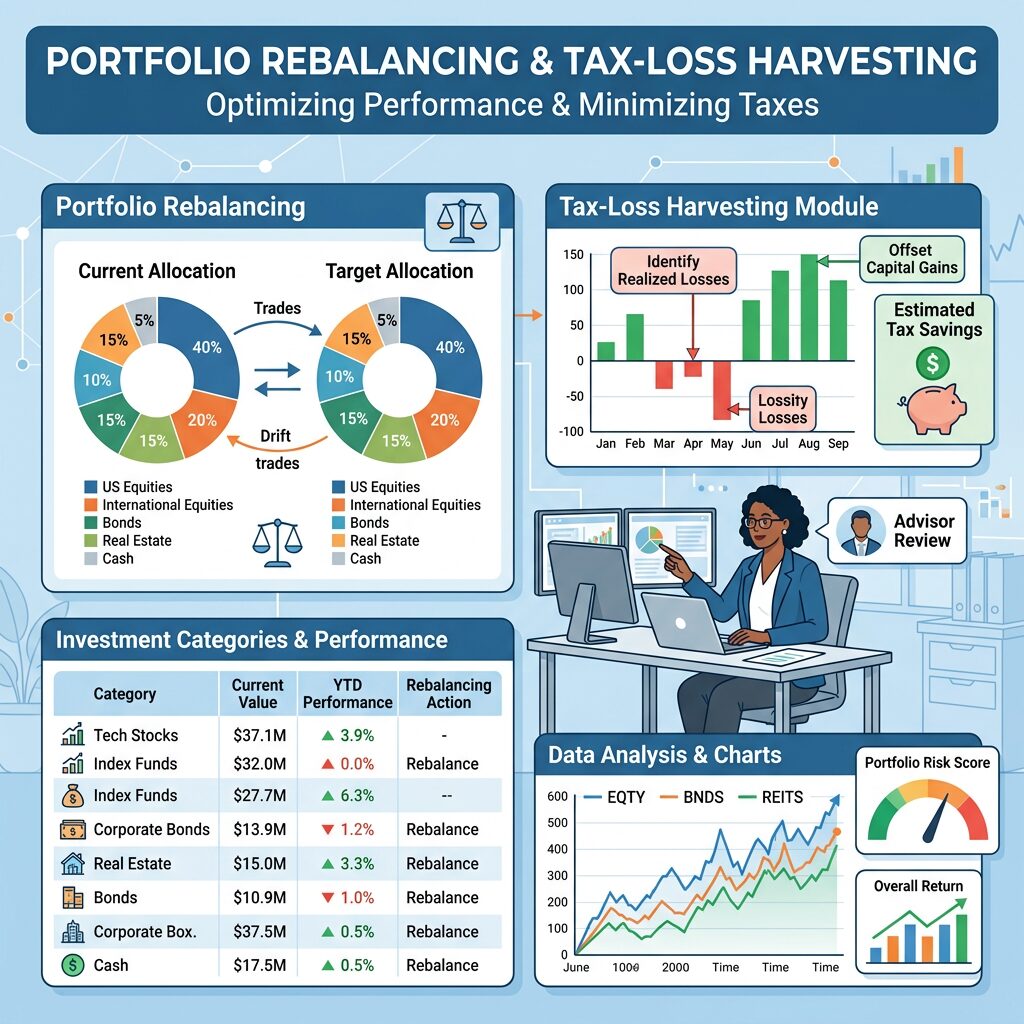

3. Tax-Loss Harvesting

Year-end is an excellent time to harvest investment losses to offset gains realized during the year.

4. Charitable Giving

Bundle charitable contributions in high-income years to itemize deductions and increase tax benefits.

5. Roth Conversions

Consider converting traditional IRA funds to Roth IRAs, especially in years when income is lower than expected.

Coordinating with Your Overall Plan

These changes are important, but they’re just one piece of your comprehensive financial plan. At Austin Wealth Management, we consider your:

– Current and projected income

– Tax filing status and family situation

– Retirement goals and timeline

– Investment strategy and risk tolerance

– Estate planning objectives

Let’s make sure you’re taking full advantage of these 2026 changes. Schedule a consultation with our team to discuss your personalized tax and retirement strategy.

More Articles

Trump Savings Accounts

The 2025 passage of the One Big Beautiful Bill Act introduced the Trump Account, a unique custodial investment tool designed to jumpstart savings for young Americans. For nearly three decades, families have relied on 529 plans...

How Portfolio Rebalancing and Tax-Loss Harvesting Help Austin Wealth Management Improve Client Outcomes

Behind every AWM advisor is a dedicated team of investment professionals meticulously looking at each client account and watching for opportunities to improve our clients investment performance...

SpaceX IPO: What Investors Need to Know

SpaceX is going public in one of the largest IPOs in history. Austin Wealth Management breaks down the valuation, the risks, and three investing scenarios — from pre-IPO allocation to long-term index exposure.